Q3 portfolio Update

Boring isn't inactive, A New Add: $TRMR, Semler Update, 4 stocks on my watchlist: $BFIT, $NEPH, $LEE, $IDXG

All performance as of 9/30

Q3 Performance: 0.63%

YTD Performance: 26.80%

Although the YTD performance is relatively strong at 26.8%, it’s been a flat Q3 (dare I tempt the gods and say boring?).

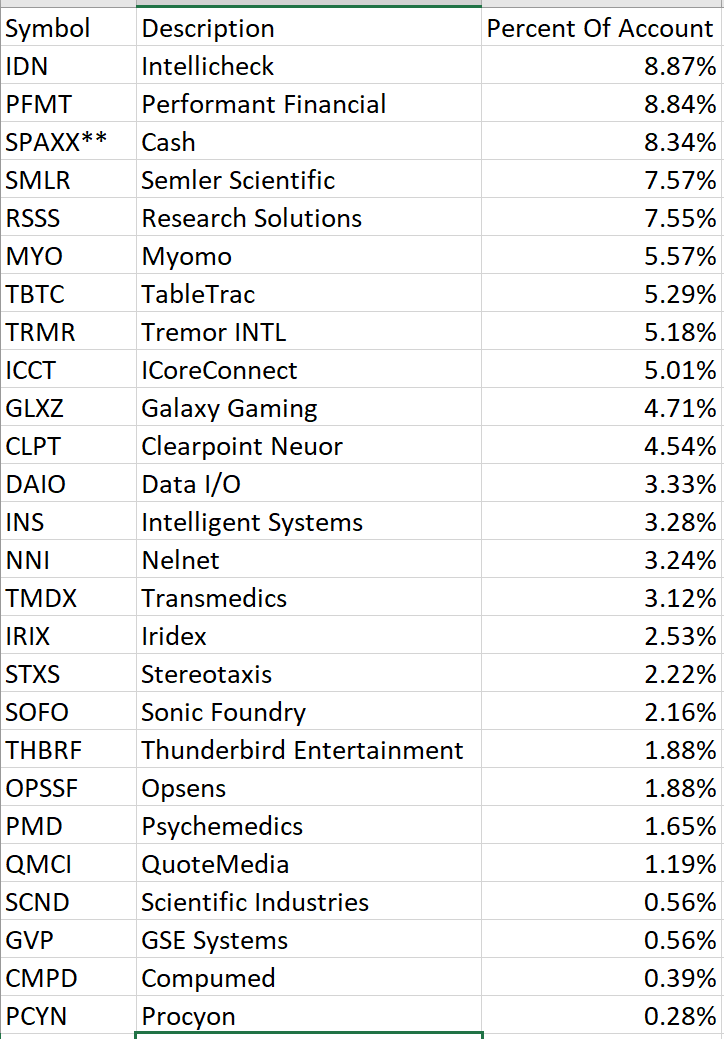

Portfolio Holdings

Additions: Tremor International, GSE Systems, ICoreConnect

Cuts: Acacia Research Group, Viemed Healthcare, Arista Networks, Redbubble.

Don’t confuse a lack of volatility with inactivity.

The third quarter was the most boring one for my portfolio to date. While there was the usual buffet of financial news ranging from supply chain disruptions to the Evergrande crisis, my portfolio (and the markets) ran in place. In fact, though I may be up 20% for the year, the gains largely came before March.

My portfolio for 2 quarters have been extensively boring with respect to overall price action, but this range-bound lack of volatility need not be confused with passivity. It's a time of continuing diligence, consuming relevant news, and evaluating new companies. As a part-time investor with the technical analysis skills of an ape and a desire to concentrate my portfolio, the bar to clear for any company to enter the portfolio is often high. It takes time to understand a company enough to be comfortable to enter into a sizable position. Even then, the timing may be early so I'll spend months waiting for the market to realize a thesis. In the intervening time, I do little but more research. One can go months without finding a good company or my stocks moving significantly. It's boring.

This is why 2-4 year, concentrated investing is difficult. One can neither get the dopamine hit of constant trading nor the flexibility afforded by 'forever' time periods. I'm constantly researching with minimal dopamine payoff.

Investing this way can feel Sisyphean. For the uninitiated, Sisyphus was cursed by the gods to roll a boulder up a hill only for it to roll back down, for all eternity. Akin to Sisyphus, I often research new companies only to find the stock unattractive. The rock rolls back down the hill. We start again. But I find solace in this often fruitless endeavor because each hill I climb accumulates my investing knowledge, preparing me to climb another one.

Even if tedious, my endeavors are distinct from Sisyphus because there is a light at the end of the tunnel. We find a stock which lights up our eyes and satisfies every criteria. It's why I can tolerate quarters such as the most recent one with little price action to keep me occupied.

The middle half of 2021 was a series of hills climbed. Eventually, the markets will recognize the underlying value of the businesses. Do not confuse boring returns with inactivity and do not let boredom push you away from doing the work. Keep searching for the next investment, doing continuing diligence, even if it feels futile in the moment.

Portfolio Review:

Key Add: Tremor International (TRMR)

Tremor Is an end to end ad tech platform housing both an SSP and a DSP focused on Video/CTV advertising. While companies like The Trade Desk and Magnite are either a DSP or SSP, Tremor owns both sides. By owning both sides of the platform, they can have a higher take rate and improve efficiency in the process. I'll spare you rewriting what has already been written on Twitter:

. There are plenty of smart people who have discussed the company on Twitter concisely and well. I can’t believe the platform is free.

In a nutshell, Tremor is strategically advantaged from both a margin and growth perspective as they can leverage data to drive better results while staying profitable. Though some see owning both sides as a conflict of interest (customers won't get the best deal), I would push back saying they don't own the inventory so this isn't comparable to the FB/Google example. Tremor merely cuts out the ridiculous number of middlemen for advertisers and publishers.

I'm trying not to overthink the thesis so I'll let the following table tell the story:

Tremor is growing their topline 30% with a rapidly growing CTV division (>100% growth). They are well positioned in a new world of ad regulation by having better access to publisher data and the possibility to offer better pricing through margin efficiencies. The company offers 100% upside based solely on revaluation to peer multiples while being a long term growth play.

Why this opportunity exists: Tremor isn't without some hair. It was originally combined with Telaria SSP until it was spun out into Tremor Video. It then went through a series of acquisitions (RhythmOne and Unruly SSP) to build the platform they have today. The business history isn't clean with the former CEO even implicated in fraud dealings ( though I would unrelated to the current business). In addition, they reclassified their revenue last year to recognize net instead of gross revenue (total money going through the platform) leading to a drop in sales. The temporary drop in revenue looks bad for anyone screening through companies without digging deeper. It was an AIM-listed company and people may not trust buying a foreign company. They listed on the NASDAQ to close the valuation gap but the stock hasn't moved since the listing.

I often overthink investments, but I don't want to overthink this one. Fast growing player in a hot space held down for arbitrary reasons. Multiple revaluation should be the first driver of stock returns while continued growth will be the second. They will continue to use piles of cash to acquire companies to build a more complete platform. The margin of safety is high given the low relative valuation. The thesis is simple and straightforward

$SMLR Update: Semler Scientific remains one of my largest holdings even after the recent 25% drop. Their home testing market had some demand pulled forward into the first half of the year which hurt their 3Q earnings (specifically from their 2nd largest customer). Management commentary wasn’t clear and could worry some investors, but it is still short term noise. They have always viewed the business as a YoY business. I expect their flagship product, QuantaFlo, to continue to perform well in the coming years as they become standard of care.

However, a response to a question about deceleration within their current customer base is concerning. It is natural to expect a deceleration in growth as each incremental patient tested naturally leads to a lower ROI. Essentially, it’s easy to identify which patients benefit the most, but the next patients are harder to identify. I plan on talking to management to see what thoughts they have on this front.

They have signed a contract for one of their ancillary products which keeps them on track for a late 2021/early 2022 rollout as expected. Gah, patience is a bitch.

Ultimately, I’m not a buyer on the dip because it’s still at >10x sales, but they continue to perform well and execute on expansion plans. I find it hard to sell a business growing 40% a year at 30X EV/EBIT, especially with a long runway for growth.

What I'm Watching:

Fund letters are often a great source of new ideas, but since I publish my exact holdings and write about most companies I own, I'm going to try something slightly different. I have a list of companies I'm watching but I haven't pulled the trigger on. Let's go through a watchlist

#1: Basic Fit (BFIT),Gym Owner in Europe: When I hear someone smart discuss a company in an industry I know, I get interested. I initially became interested in the company after reading David Polansky's letter in July 2021. Adam Wilk then wrote about the company on his Q3 investor letter. Gyms are a great business to own since people rarely churn. They're essentially a tax on people's desire to be fit. The margins are high and the runway to growth is long. Based on a valuation laid out by both investors based on continuing gym openings and per gym profits, the stock has serious upside.

Why don't I own it? Not enough diligence. I need to do more work on the name to own it. Specifically, I want to learn more about the company history, the European market for gym goers and the quality . In addition, I need to model out future growth for myself for a sanity check.

#2: Nephros (NEPH), Water Filters For Hospitals: The company was growing 50%+ before COVID which hit them pretty hard given their primary customers are hospitals. Insiders own a significant chunk and the company has introduced a new of products which nicely complement the water filters. New laws requiring water filtration in hospitals benefitted the company for the past couple years but there is still room to grow

Why don't I own it? With 50% gross margins and at 8x sales, I'm concerned about the valuation. In my opinion, they are limited in the possible profitability due to the gross margin. I'm waiting for the stock to drop for it to become a 'fat pitch'. This could certainly come back to bite me as an error of omission.

#3: Lee Enterprises (LEE), Legacy Newspapers Transitioning to Digital: Plenty has been written on Seeking alpha about the company so I encourage you to look at that. It’s a newspaper company with a growing digital subscriber base. There is an absolute metric ton of debt though management believes it is manageable with current operations. I have read poor reviews about the company's assets, but local news is a tough business. If it can repay the debt and morph into a digital first company, they have the opportunity to be a multi-bagger.

Why don't I own it? Owning a melting iceberg like local newspapers means there isn't as much margin for error. Valuation isn't demanding, but I'm unclear on the dynamics of local news and how much of their digital subs can grow. I need to model out debt repayment as well to become comfortable owning it.

#4: Interpace Diagnostics (IDXG), Molecular diagnostics for Pancreatic and Esophageal Cancer. It’s owned by renowned investor Peter Kamin and recently restructured becoming increasingly profitable. They brought in a new CEO and acquired a business which sells to pharma companies. With less than a 3x EV/Sales and a large TAM, this looks like an amazing stock though competitive advantages of the different tests are unclear. They recently received and increase in reimbursement which positively impacted revenue for the pancreatic testing segment.

Why don't I own it? Their new tests are unproven and there are competing tests for the main pancreatic cancer product. In addition, I've tried to contact the companies multiple times with no response at all. Their products need more validation for insurance reimbursement though having strong private equity (Ampersand and 1315 Capital) and public markets (Kamin) investors lends them some credibility.

Nice rebrand of the substack Adu, you definitely have strength in this niche. Luke