The business is very simple: they sell construction equipment. They have two primary lines of revenue soft goods, which include pouches and tool belts, and metal goods, like sawhorses. Their target audience are DIY builders and professional construction workers. For many goods (since they are shipped from Asia) they partner with Belegal, a Chinese industrial company for quality control and shipping goods manufactured in Asia. There isn’t a technical moat, but management says their competitive advantages stems from an ability to respond to customers needs quickly and their brand name. even though, TBLT sells construction goods, the small cost and DTC nature of their business makes them more akin to a consumer goods company. As with any consumer goods company, the product and brand name is the most important part of increasing sales.

Products and Reviews: Management cites their product line as part of their competitive advantage and the reviews live up to the hype. According to reviewmeta, a review aggregator, their products on amazon have an overall rating of 4.5.

60

Products Analyzed

6% of potentially unnatural

reviews removed (%0?)

3,059

Reviews Analyzed

ReviewMeta

average adjusted rating

2,890 Reviews

See products")

The number of reviews is especially impressive, because they only recently launched the amazon storefront in mid 2019. In addition, 74/78 of their products on Home Depot online have reviews above 4 stars. They hold some patents on their various designs, but rely a lot on quality designs at bargain prices. A quick search for Toughbuilt reviews on Youtube will show you how well liked the products are and the comments are especially positive. As they build a brand, their sales will accelerate. Their products are clearly catching on as Lowe’s recently signed a deal with Toughbuilt to award them all of the kneepad business and a portion of soft sided tool storage business (i.e. tool pouches). The deal was to be launched in October of last year with a project annual sales of $22.7 million.

Financial Performance: Toughbuilt Recently saw an acceleration in revenue in Q320 with QoQ growth of 248% and 88% growth from the 9 month period from the previous year. In addition, the company turned profitable (albeit barely) for the first time in the quarter. The large growth seen in Q3 can be attributed to a couple of reasons, Amazon sales, and the introduction of a new customer, likely Lowe's. The Lowe's deal was an especially positive number for the quarter as they shipped a bulk order of goods in August 2020 to begin the partnership.

Amazon storefront - After launching in 2019, the gross sales for the Amazon storefront in FY20 was $7 million with the following quarter numbers pieced together from various press releases.

Q420: 2.38, run rate of 9.52 million, growth of 15% sequentially, and 65% YoY.

Q320: 2.07 mil

Q220: 1.35

Q120: 1.2

First 8 months: 2.5 million

Q419: 1.44

By setting up the storefront before the pandemic, Toughbuilt was prepared for the lockdowns and sales were resilient.

Margin Profile - The gross margins are around 45% and improving due to increasing efficiencies in the production process. Management has guided for continued margin growth as R&D spend will stay constant on a dollar amount and sales will continue to grow. At scale, construction companies like Caterpillar have a net margin of ~6% and I would expect TBLT to have a larger margin because of their brand name and consumer goods nature of the business. They have established partnerships and a growing brand, thus their SG&A costs will scale at a lower pace than revenues over time.

Future Growth:

Suburb explosion: Homebuilders have been on fire this year as demand for suburban housing has exploded. This isn't a temporary shift as the conditions for this explosion were demographically set before the pandemic. I highly recommend this podcast with Josh Brown and Logan Mohtashami about why the COVID housing boom isn't an anomaly. As more houses are built and more people have houses to work on, Toughbuilt sales can continue to grow.

International expansion - currently they derive ~80% of their sales from the USA, but good construction gear is international. As they scale, they can grow into other markets.

Mobile App and devices - I put this one last, because it is both a growth opportunity and a red flag. Toughbuilt has discussed developing a 'rugged mobile device' for construction workers and corresponding apps to help workers since 2017. In 2019, they received a patent for their mobile device and a prospectus filed recently says they “are planning to have our mobile device products ready to market in first half of 2021” . However, color me skeptical as management has made similar claims in the past regarding app developments: they “announced the planned launch of a suite of new applications designed for the licensed contractor market, which launch is expected to occur in late 2019.” Note that these statements were made before any Covid-19 related disruption. Since I couldn’t find any evidence of their apps on the appstore, online, or any revenue in SEC filings, I contacted the investor relations and they said developments on the device/app would be coming 'soon' and through a press release. After years of touting a potential device and software, I find it hard to believe they would be on schedule to release this device and without any earnings calls or analysts covering them, I am skeptical about some of their claims. In addition, no marketing has been done yet with an expected release in the 1H21. However, if they do announce a phone/apps, the stock would likely jump as people looked at the news as evidence that management was started to deliver. In addition, the potential for a specialized phone/apps could be big.

Risks:

Inability to iterate - the biggest risk is the most obvious one: they fail to continually innovate and their products go out of style. This risk will always exist for any company especially in a consumer goods space

Cyclical products - Their sales in the past have had lumpy growth rates that ebb and flow with the market demand for DIY projects. We are currently in a boom cycle so their growth rates are high, but cyclicality for their products could return and depress sales growth in the following years. One mitigant of this risk could be that their products are just now being scaled up and penetration of the market will mask any cyclicality

Customer/supplier concentration - They also have a significant supplier and customer concentration with their top four customers and suppliers making up more than 20% and 30% of their sales and supplies respectively. I am not concerned with the customer concentration because there are a limited number of hardware distributors In the US (Home depot, Lowe's, etc), but the supplier concentration could come back to bite them if one of their suppliers cuts off the relationship or starts to raise prices.

Lack of visibility into the company - the biggest downside of the company is the lack of visibility with a close second being the lack of insider ownership. I group these together because they could signal a company that exists solely to issue stock whose management doesn't believe in the future of the company. They host no earnings calls which is puzzling and the investor relations department didn’t indicate that they were going to start doing so anytime soon. There has been a modest amount of executive turnover in recent with two people leaving in the last two years but the company is founder led. Overall, the corporate governance makes this company very opaque and difficult for me to evaluate. Their products are legit so I wonder why management isn't more forthcoming with information. In addition, even though it is a founder led company, the insider ownership level is less than 5%. In addition, The CEO also suspiciously made nearly 1 million dollars in 2018 (with nearly $50,000 for “Vacation Payout and other”) which is higher than I would like for a CEO of a money losing microcap company.

Lack of adequate cash - The company has 8 million of cash on the balance sheet and burned 20 million in cash in the past twelve months. They have filed for an offering of up to $100m in shares which would seriously dilute the stock at current levels. They diluted shareholders heavily in the past year through issuing $28 million in equity.

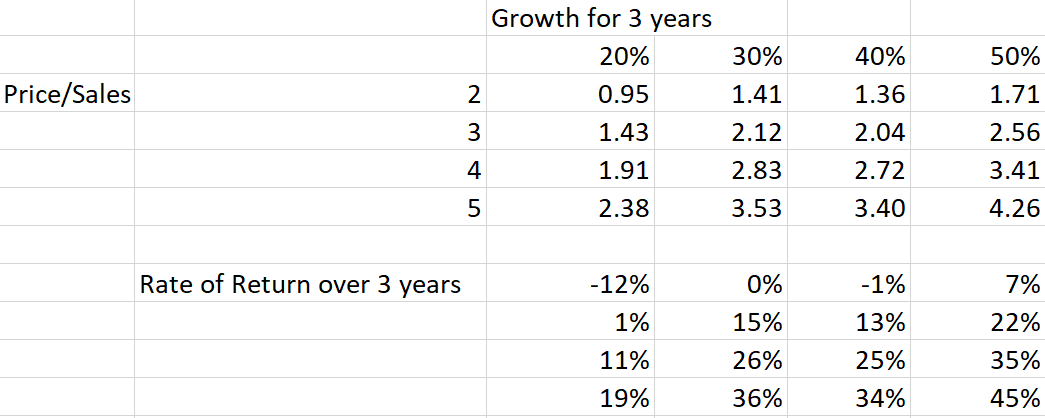

Valuation: Based on Q3 results, we would expect them to do ~33 million in sales for FY 20 which would be growth of 80%. They have an EV/Sales of 1.88 with a gross margin of ~40%. Their EBITDA Margin for the last year is -21.8%. Based on Q3 results we can also say they need 16 million in a quarter to be profitable. We can see that with a 50% growth rate, they still only reach profitability by the end of 2022. To sustain them for the next three years, they will likely have to issue stock which would dilute shareholders to the tune of $60 million dollars. This puts the number of shares outstanding (diluting at $1.40) at 103 million by 2022. Assuming the stock trades at 3x Sales with 25% sales growth, a reasonable valuation given the consumer goods nature of the company, the market cap is 180 million and the share price is 1.80$.

I have done the following sensitivity analysis assuming the following: FY20 sales = 32 million, Breakeven is $64 million in a year, they need to dilute to get $20 million a year in cash, and their share price is 1.4 at issuance. A lower share price would mean the returns would be even lower (it is currently trading at 1.12).

We are looking at a max CAGR of 45% and a likely rate of return in the 10-20% range if everything goes well.

Conclusion: Overall, this company is extremely underfollowed and in a 'boring' industry. The current products are legit and they have partnerships with established players in the field. However, a combination of a lack of visibility, negative profitability, low insider alignment with shareholders, and no execution on new products prevents me from having any conviction to invest. The company spooks me on a number of fronts due to the complete lack of execution even though they sell good products. If it wins big, I would expect to be able to see the signs early and act appropriately since the company is sorely underfollowed. If they corrected or minimized any of the risks (hosting earnings calls, releasing a phone, etc. ), I would re-evaluate at that point.