What are the Chances?

How likely is it that you have chosen a winning stock? Stock picking as a diagnostic test.

The recent underperformance of fintwit growth favorites has washed away the many performance posts and rocket ships seen through much of last year and early this year. 'Growth at any price' isn't a common investing mindset as even nascent investors have heard of valuation and ****gasp**** profitability, but people are enamored with growth and often regard valuation as a red-headed stepchild. People are willing to pay up for supposed quality. In the throes of earnings season, a brief non-stock related post seems appropriate. This week, I wanted to look at how valuations can affect your returns through a lens of medical diagnostics (or if you’re fancy, Bayesian statistics) and how these can frame the chances of picking the 'next Amazon'.

It goes without saying that relatively high valuations (historically speaking) lead to underperformance of the market in aggregate, but if one is an excellent analyst, is underperformance inevitable? When you can find the next great compounder, why should market underperformance matter? There are certainly great companies that will survive and thrive in all types of markets. True compounders can compound wealth over a generation regardless of market direction.

Investors aren't simply making levered bets on market direction when buying high growth companies: they are supposedly buying the next generation of Trillion $ businesses. Buyers of The Trade Desk believe it will play a role in the massive shift to connected TV. Shopify buyers are betting it will be the go-to E-Commerce company in a world moving online. Tesla is the future of electric vehicles, autonomous driving, car insurance, space and batteries. As the canonical example goes, they are buying the next Amazon and, if discount rates are low, one can buy high growth at high valuations (though Amazon hasn't traded above 7x sales since the tech bubble).

If you had bought Amazon at the peak in 1999 at 100$ a share (>40x Sales), you would still compounded your capital at >17% over 21 years and would be sitting on a >30x bagger. Not too shabby. Packy McCormick framed investor thinking well, coining the price-FAAMG ratio: with discount rates so low "you can abstract away a lot of complexity by thinking about startup valuations as the probability that they can grow as large as Facebook, Amazon, Apple, Microsoft, or Google." When the end result is a trillion dollars, people are willing pay up.

I know some value investors immediately rolled at their eyes at that take, but he has a point. If CRISPR is going to change medicine, why wouldn't I pay up in form of a 25x P/Sales ratio? The issue with high valuations comes in two forms: 1) you must be extremely good at picking stocks due to a decreasing prevalence of stock winners at high valuations 2) high valuations reduce the likelihood of having a generational winner make up for a portfolio of duds.

A trip is Bayesian Statistics: Sensitivity, Specificity, PPV, NPV

Let us take a trip out of investing to look at a useful framework from the perspective of a medical diagnostic test using sensitivity, specificity, positive predictive value, and negative predictive value.

Say we test everyone for COVID 19. The sensitivity is the amount of people with the disease who would test positive, thus a high sensitivity means few false negatives. In the same vein, the specificity is the number of people without the disease who test negative (high specificity means few false positives)

Now the positive predict value (PPV)/negative predictive value (NPV) are different. A PPV is the chance you have the disease if you receive a positive test and a NPV is the chance that you don't have the disease if you get a negative test. While the sensitivity and specificity are solely characteristics of the effectiveness of the test, the PPV/NPV are affected by prevalence of the disease. The equations relating the variables are on the Wikipedia page with a nice explanation.

I tried to make the explanation as simple as possible but if you’re still iffy on the topic, there are some great videos and articles on the topic out there.

Back to Investing

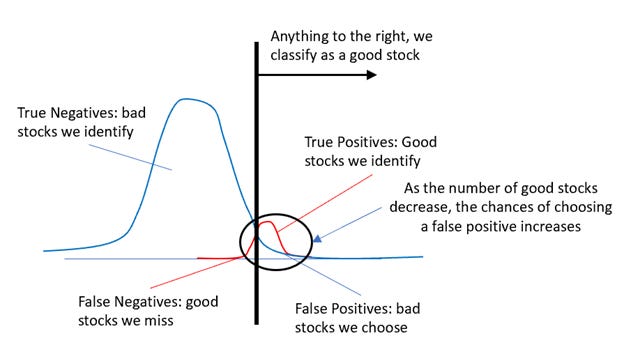

With that quick tangent out of the way, let’s tie it to investing. The sensitivity and specificity are only functions of the stock picker. Assuming a 'positive stock' is good stock, a highly sensitive stock picker doesn’t miss many good stocks (reducing false negatives) while a highly specific stock picker doesn’t pick many stocks that lose (reducing false positives). The PPV in terms of investing are the chances that a stock pitch is actually successful. (i.e. I pitch a stock, the chances that the stock works is the PPV, akin to a ‘batting average’).

However, problems arise regarding the PPV/NPV when factoring in the prevalence of good stocks. In a high valuation environment, the prevalence of winning stocks drops (more room for multiple compression). As the prevalence of winning stocks drops, what happens to the chances that a certain stock pitch will be right (the PPV)?

Say you are 95% sensitive and 95% specific which is phenomenal as a stock picker. This means you could identify 95% of winners and 95% of losers given the companies you analyze. Say 1% of stocks are real winners, the chances that a stock you choose will be one of those winners is 50%. Every stock you pick is a coin flip on whether it will succeed.

We can generate the following the table for a 1% prevalence of good stocks.

Amazing! The max possible chances that a stock you pick will be a winner is a coin flip.

Some may argue that the increasing pace of disruption means the prevalence of long-term compounders are increasing thus increasing the likelihood of choosing a winner. But let us move the prevalence up to 10% and see what happens to the table.

A stock picker who correctly identifies 90% of winners and 90% of losers still only has a coin flip chance.

If you want to play around with the prevalence number, you can check out this google sheet

What about slugging percentage?

Now, these stats are all batting average stats (% of stock choices that work well), but many investors don’t care about batting average: they want a high slugging percentage. It’s ok to hold a portfolio of zeros if a single company can compound its capital at 30%. One generational winner is life changing.

However, the bane of valuation reels in our hopes once again. Buying Amazon at the peak as a 30x bagger is much different than buying amazon after the crash for a 500x bagger. Without room for multiple expansion, truly mind-boggling returns are hard to come by.

One can buy the next Amazon and still not beat their benchmark.

How can we help ourselves?

Now, how can we help ourselves and increase our batting average?

Reduce False Positive (increase our specificity): Let's go back to the PPV table. If you look at the table, what really affects the PPV isn't the sensitivity (the chances of finding a good stock), it is the specificity (the chances of identifying bad stocks). To increase our PPV, we must reduce our false positive rate. An easy way to do this is to swing at less pitches. Also, we can only invest in companies after extensive research. One can obviously discuss diversification to reduce susceptibility to company specific risk and reduce volatility, but from a purely stock picking perspective, swinging less and with more conviction leads to an increased rate of success both increasing specificity and PPV. Seems obvious, right?

Fish in Better Ponds: One way to frame systemic value investing is as a bet on these Bayesian models. By choosing cheap stocks, these baskets are investing in a pool of stocks with a higher prevalence of positive returns over 3-5 years due to mean reversion. The same logic holds for us individual investors: fish in ponds where winners are prevalent. Whether its microcaps, international stocks, or unloved sectors, there are places out there where the rate of winners can be higher due to low valuations and minimal attention. By investing where the prevalence of good stocks is high, we do not need to be a great analyst! It is like buying stocks in March 2020 for 1 year, the odds were in your favor.

Summary

Every company cannot be a compounder and high valuations reduce both the chances of finding the next great company and the positive impacts of finding it. Even if the rate of disruption is increasing introducing more generational winners, high valuations pare your returns. If one wants to be better at picking stocks, swing less and invest in areas where the odds favor you.

crisp analysis

Great write-up. May the odds be in your favor.